The Smith Manoeuvre is a legal Canadian tax strategy that converts non-deductible mortgage debt into tax-deductible investment debt by using a readvanceable mortgage to borrow against your home equity and invest those funds into income-producing assets. Named after financial planner Fraser Smith, the strategy is governed by section 20(1)(c) of the Income Tax Act, which permits Canadians to deduct interest on money borrowed to earn investment income. For Alberta homeowners carrying a mortgage, this means your largest monthly expense can start working toward building a taxable investment portfolio while reducing what you owe the Canada Revenue Agency (CRA) each year.

How does the Smith Manoeuvre work in Canada?

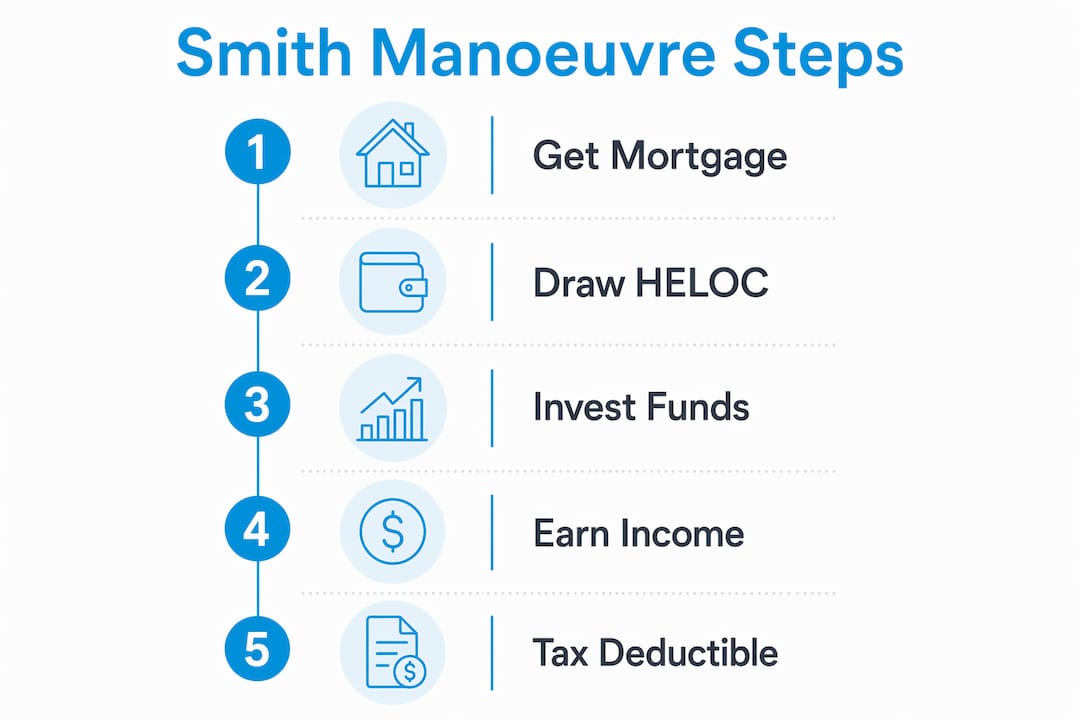

The Smith Manoeuvre works through a readvanceable mortgage, which combines a standard mortgage with a home equity line of credit (HELOC) in a single product. Each month, your regular mortgage payment reduces your principal. That reduction automatically increases your available HELOC room by the same amount. You then borrow that newly available amount from the HELOC and invest it immediately into income-producing assets.

The cycle repeats every month. Over time, your mortgage balance shrinks while your HELOC balance and investment portfolio grow in parallel. The interest you pay on the HELOC is deductible on Line 22100 of your tax return, because the borrowed funds are used to earn investment income. Your annual tax refund then goes back toward the mortgage, which accelerates the whole process.

Here is how the monthly cycle works in practice:

- Make your regular mortgage payment. Principal repayment increases your available HELOC limit.

- Borrow from the HELOC. Draw the exact amount your principal decreased.

- Invest the borrowed funds. Purchase income-producing assets such as dividend-paying ETFs.

- Claim the HELOC interest. Deduct it on your tax return under Line 22100 as investment interest.

- Reinvest your tax refund. Apply the refund as a lump-sum mortgage payment to speed up conversion.

Accelerated versions of the strategy reduce the total conversion timeline by 6–8 years compared to a standard 20–25 year amortisation period. That is a meaningful difference in how quickly your mortgage debt becomes fully deductible.

Pro Tip: Keep a dedicated HELOC sub-account used exclusively for investment borrowing. Never mix personal spending with this account. Commingling funds is the single fastest way to lose your interest deduction entirely.

Who qualifies for the Smith Manoeuvre?

Not every Canadian homeowner is a good fit for this strategy. The CRA sets clear conditions, and meeting them requires both financial preparation and long-term commitment.

The recommended starting point is at least 20–25% home equity. You also need stable income and a long investment horizon of 15 or more years. Without those two conditions, the strategy carries more risk than reward.

Key eligibility and compliance requirements include:

- Readvanceable mortgage. Your mortgage product must automatically increase your HELOC limit as you repay principal.

- Income-producing investments only. The CRA requires borrowed funds to be invested in assets that generate dividends or interest, not capital gains alone.

- Separate HELOC account. Each advance must be traceable to a specific investment purchase.

- No registered accounts. Funds invested in an RRSP, TFSA, or FHSA do not qualify for interest deductibility under section 20(1)(c).

- Proper documentation. Logs of each advance, the date, the amount, and the investment purchased are required for audit defence.

CRA's position is clear: interest is only deductible when there is a direct link between the borrowed money and an income-earning investment. If that link breaks, the deduction disappears. At a 40% marginal tax rate, $10,000 in HELOC interest generates roughly $4,000 in tax savings. That number drops to zero if your records do not hold up.

The Smith Manoeuvre is not suitable for homeowners with unstable income, high consumer debt, a low tolerance for market risk, or a short homeownership timeline. Those factors make the strategy financially dangerous rather than beneficial.

What are the risks of the Smith Manoeuvre?

The Smith Manoeuvre amplifies both gains and losses because you are investing borrowed money. That is the core risk, and it deserves a clear-eyed look before you commit.

Rising interest rates directly affect the strategy's feasibility. When HELOC rates climb from 4% to 8%, your carrying costs double while your investment returns may not keep pace. The strategy only works when your after-tax investment return exceeds your after-tax borrowing cost. That gap can close quickly in a rate-rising environment.

Key risks to weigh carefully:

- Market downturns. Your investment portfolio can fall in value while your HELOC debt stays fixed. You still owe the full balance regardless of what markets do.

- Forced liquidation. Job loss or a credit freeze could force you to sell investments at a loss to cover HELOC payments.

- Audit risk. Poor recordkeeping or mixed-use accounts can result in CRA denying your interest deduction on the entire loan balance.

- Psychological pressure. Carrying large variable-rate debt during a prolonged market decline is frequently underestimated as a stressor. Panic selling at the wrong moment destroys the strategy's long-term value.

- Cash flow strain. You need enough monthly income to cover both your mortgage payment and HELOC interest without touching the invested funds.

Pro Tip: Build a three-to-six month emergency fund before starting. If your cash flow tightens unexpectedly, that buffer prevents you from raiding your HELOC investments and triggering a CRA audit.

The strategy demands a long-term commitment and strong financial discipline. It is not a passive set-and-forget plan.

How to implement the Smith Manoeuvre effectively

Getting the setup right from the start prevents the most common and costly mistakes. The foundation is choosing the correct mortgage product.

Not all mortgage products support automatic HELOC readvancing. Products such as Manulife One and National Bank All-In-One are designed for this purpose. Many insured mortgages lack the readvance feature entirely, which means the strategy cannot function without a product switch.

Once your mortgage is in place, follow these implementation steps:

- Open a dedicated HELOC sub-account. Use it exclusively for investment borrowing. Never use it for personal expenses.

- Select income-producing investments. Canadian dividend ETFs such as XDIV and VDY, broad equity ETFs such as XEQT, and bond ETFs such as ZAG qualify for interest deductibility. Growth stocks without dividends and cryptocurrency do not.

- Log every transaction. Record the date, HELOC advance amount, investment purchased, and price paid. This is your audit trail.

- Apply dividends to your mortgage. Redirect investment income as additional mortgage payments to accelerate principal repayment.

- Apply your tax refund as a lump sum. Each year's refund goes directly onto the mortgage, which opens more HELOC room and restarts the cycle faster.

Using dividends and tax refunds to make extra mortgage payments creates a compounding cycle that shortens your total exposure by several years. This accelerated approach demands active management but produces meaningfully better outcomes over a 15-year horizon.

The most common pitfalls are straightforward to avoid. Do not spend HELOC funds on personal items. Do not invest in assets that produce only capital gains. Do not skip monthly recordkeeping because it feels tedious. Each of these errors can result in CRA denying your interest deduction on the full HELOC balance.

Work with a mortgage broker who understands readvanceable products, a tax accountant familiar with section 20(1)(c), and an investment advisor who can select qualifying assets. Pairing the Smith Manoeuvre with maximised RRSP and TFSA contributions also ensures you are building wealth across both registered and non-registered accounts simultaneously.

Key takeaways

The Smith Manoeuvre works because it converts non-deductible mortgage debt into tax-deductible investment debt, but only when implemented with strict recordkeeping, qualifying investments, and a long-term commitment of 15 or more years.

| Point | Details |

|---|---|

| Readvanceable mortgage is required | Your mortgage must automatically increase HELOC room as you repay principal each month. |

| Investments must produce income | Only dividends and interest qualify; capital-gains-only assets and registered accounts do not. |

| Recordkeeping is non-negotiable | Log every HELOC advance and investment purchase to defend your deduction under CRA audit. |

| Accelerated methods save years | Reinvesting dividends and tax refunds as mortgage payments shortens conversion by 6–8 years. |

| Risk management comes first | Build an emergency fund and confirm stable cash flow before starting the strategy. |

What I have learned advising Alberta homeowners on this strategy

The Smith Manoeuvre is one of the most misunderstood strategies I encounter. Homeowners often come to me having read about it online and believing it is a simple tax hack. It is not. It is a long-term wealth-building commitment that uses your home as the foundation of a leveraged investment plan.

What I have seen work consistently is this: the homeowners who succeed with the Smith Manoeuvre treat it like a second job for the first few years. They track every transaction, they reinvest every dividend, and they apply every tax refund to the mortgage without exception. The ones who struggle are the ones who set it up and then stop paying attention.

The psychological side is real. Carrying a growing HELOC balance during a market correction is genuinely stressful. I always ask clients to sit with that discomfort hypothetically before we proceed. If the idea of watching your portfolio drop 30% while your debt stays the same keeps you up at night, this strategy is not the right fit, and there is no shame in that.

My honest recommendation is to pair the Smith Manoeuvre with a fully funded RRSP and TFSA before you start. The registered accounts give you a tax-sheltered cushion. The Smith Manoeuvre then works on top of that foundation rather than instead of it. That balanced approach is what I guide clients toward at Deneenoel, and it produces far better long-term outcomes than chasing a single strategy in isolation.

— Denee

Working with Deneenoel on your Smith Manoeuvre mortgage in Alberta

Setting up a Smith Manoeuvre correctly starts with the right mortgage product. Not every lender offers a readvanceable mortgage, and choosing the wrong structure means the strategy cannot function as intended.

At Deneenoel, we work with Alberta homeowners in Edmonton, Calgary, and surrounding communities to find mortgage products that are compatible with the Smith Manoeuvre. We take the time to explain your options clearly, match you with lenders who offer readvanceable structures, and make sure your mortgage is set up to support your long-term financial goals. Whether you are in the early planning stage or ready to move forward, our Alberta mortgage services are here to guide you through every step with patience and care. Reach out to explore what is possible for your situation.

FAQ

What is the Smith Manoeuvre in Canada?

The Smith Manoeuvre is a Canadian tax strategy that uses a readvanceable mortgage to convert non-deductible mortgage interest into tax-deductible investment interest under section 20(1)(c) of the Income Tax Act. Borrowed HELOC funds are invested in income-producing assets, and the interest is claimed on Line 22100 of your tax return.

Is the Smith Manoeuvre legal in Canada?

Yes, the Smith Manoeuvre is fully legal. It relies on a long-standing provision of the Income Tax Act that permits interest deductibility when borrowed money is used to earn investment income, provided the CRA's documentation and tracing requirements are met.

What investments qualify for the Smith Manoeuvre?

Investments must produce income such as dividends or interest to qualify. Canadian dividend ETFs like XDIV and VDY, broad equity ETFs like XEQT, and bond ETFs like ZAG are eligible. Growth stocks without dividends, cryptocurrency, and investments held inside registered accounts do not qualify.

How long does the Smith Manoeuvre take to complete?

The standard conversion period follows your mortgage amortisation, typically 20–25 years. Accelerated versions that reinvest dividends and tax refunds as extra mortgage payments can shorten that timeline by 6–8 years.

Can I use the Smith Manoeuvre in Alberta?

Yes, the Smith Manoeuvre applies across Canada, including Alberta. Alberta homeowners in Edmonton and Calgary can access readvanceable mortgage products through brokers like Deneenoel who specialise in tax-efficient mortgage structures.