Debt consolidation with a mortgage is the process of combining multiple high-interest debts into a single mortgage payment secured by your home equity. For Alberta homeowners carrying credit card balances, car loans, or lines of credit, this approach, formally called mortgage-backed debt consolidation, can meaningfully reduce monthly payments and simplify finances. The three main methods are mortgage refinancing, a Home Equity Line of Credit (HELOC), and a second mortgage. Each works differently, costs differently, and suits different financial situations. Understanding which one fits your circumstances is the first step toward real mortgage debt relief.

How does debt consolidation through mortgage refinancing work in Canada?

Mortgage refinancing replaces your existing mortgage with a new, larger one. The difference between the old balance and the new loan pays off your other debts. A HELOC gives you a revolving credit line secured against your home equity, which you draw from as needed. A second mortgage sits behind your primary mortgage and provides a lump sum at a higher rate.

In Canada in 2026, consolidation rate ranges differ significantly across these products. Refinancing sits at 4.15%–4.85%, HELOCs at 4.95%–5.45%, and second mortgages at 6.5%–12%. All three options cap combined borrowing at 80% of your home's appraised value. That ceiling matters more than most homeowners expect.

What the 80% LTV limit actually means for you

Many homeowners assume they can access 80% of their home's value as new cash. In reality, only the difference after subtracting your existing mortgage balance counts as accessible equity. If your home is worth $600,000 and you owe $450,000, your maximum borrowing room is $30,000, not $480,000. That gap surprises a lot of people and changes the math entirely.

The stress test and its effect on qualifying amounts

Federal OSFI rules apply the B-20 stress test to all refinances and HELOCs. Lenders qualify you at your contract rate plus 2%, or at 5.25%, whichever is higher. This reduces the amount you can borrow by roughly 15%–20% compared to what the rate alone would suggest. If you are already carrying significant debt, the stress test may limit your consolidation amount more than you expect.

Pro Tip: Run your numbers before you apply. Use your current mortgage balance, your home's current market value, and your total debts to see whether enough equity exists to make consolidation worthwhile.

The key distinction between secured and unsecured debt matters here. Credit cards and personal loans are unsecured. Rolling them into your mortgage makes them secured against your home. That shift changes the consequences of missed payments significantly.

What are the costs, risks, and qualifications for consolidating debt with your mortgage?

Qualifying for mortgage-backed debt consolidation requires meeting specific thresholds. Most A-lenders in Canada require:

- A credit score of 680 or higher

- A total debt service ratio (TDS) of 44% or less

- Two or more years of stable, documented income for self-employed applicants

- A property appraisal confirming sufficient equity

Meeting these thresholds gets you access to the best rates. Falling short pushes you toward B-lenders or second mortgage options, both of which carry higher rates and fees.

Costs you need to budget for

Refinancing is not free. Typical costs include lender fees of 1%–3% of the loan amount, appraisal fees of $300–$500, and legal fees of $500–$1,500. On top of those, prepayment penalties on fixed-rate mortgages can range from $3,000 to $18,000 or more. That penalty alone can erase months of interest savings.

Mortgage professionals use the payback test to assess whether refinancing makes sense. You divide your prepayment penalty by your annual interest savings. If payback exceeds 18 months, a HELOC or second mortgage is likely the better path. This single calculation prevents many costly mistakes.

The risk most homeowners underestimate

Converting unsecured debt to secured debt is the most serious risk in this process. Credit card debt, if unpaid, damages your credit score. Mortgage debt, if unpaid, can result in foreclosure. Your home becomes the collateral for what were previously unsecured obligations. That is a meaningful change in risk profile, and it deserves serious consideration before you sign anything.

Refinancing also extends your amortization. Consolidating short-term credit card debt into a 25-year mortgage lowers your monthly payment, but dramatically increases total interest paid over the life of the loan. A lower rate does not automatically mean a lower total cost.

What strategies improve success with mortgage debt consolidation?

Consolidation only works if your spending habits change. Continued credit card use after consolidation leads to double debt: the new mortgage balance plus fresh credit card balances. That combination increases foreclosure risk and leaves you worse off than before.

The following strategies protect your financial position after consolidation:

- Stop using credit cards for discretionary spending immediately after closing

- Build an emergency fund of $5,000–$10,000 before relying on credit again

- Set up accelerated bi-weekly mortgage payments to reduce total interest

- Make lump-sum prepayments whenever possible within your mortgage's prepayment privileges

- Reduce credit card limits after consolidation to lower the temptation and your TDS ratio

Pro Tip: Accelerated payments and lump-sum prepayments are the most effective tools for avoiding decades of extra interest when rolling consumer debt into a long amortisation. Even an extra $200 per month makes a measurable difference over a 25-year term.

When consolidation is not the right fit, a consumer proposal may be the better option. Consumer proposals suit homeowners with poor credit, unstable income, or insufficient equity who cannot qualify for mortgage-based solutions. They protect your home while restructuring debt without adding secured obligations.

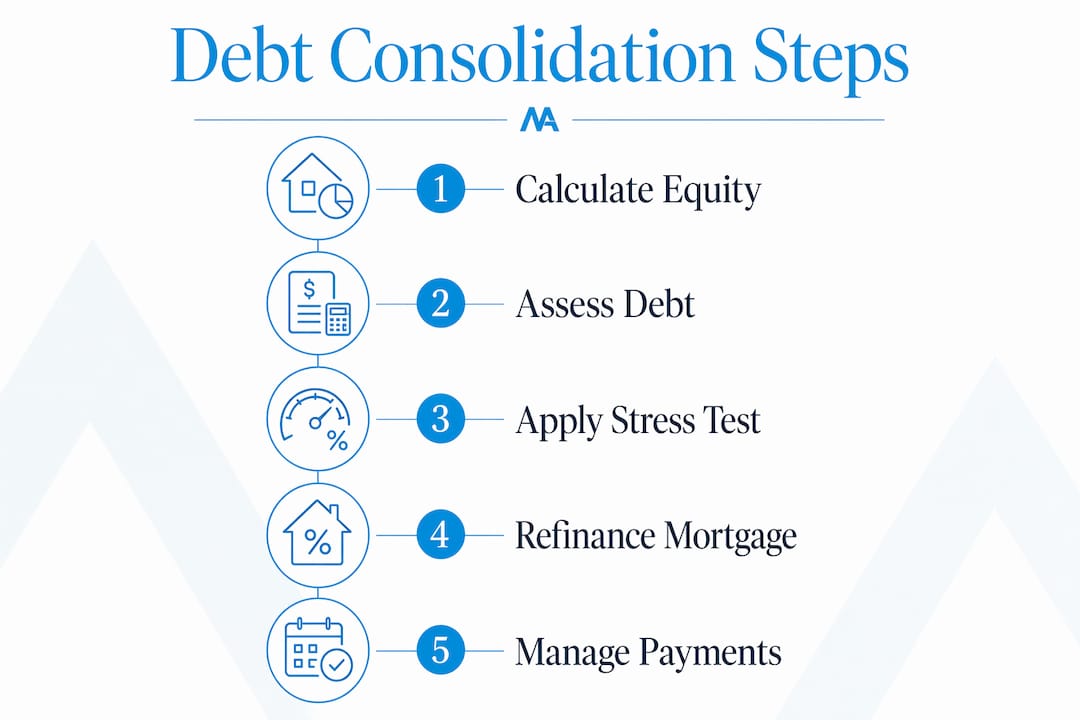

Step-by-step guide to consolidating debt with your mortgage in 2026

Working through this process in order prevents costly errors and missed deadlines.

-

Calculate your available equity. Subtract your current mortgage balance from 80% of your home's appraised value. That figure is your maximum borrowing room.

-

Get a mortgage penalty quote. Contact your lender and ask for the exact prepayment penalty in writing. For fixed-rate mortgages, this is typically the greater of three months' interest or the Interest Rate Differential (IRD).

-

Run the payback test. Divide the penalty by your projected annual interest savings. If the result is under 18 months, refinancing is worth pursuing. If it exceeds 18 months, compare HELOC and second mortgage options.

-

Compare your three options. Use the rate ranges and your equity calculation to model each scenario. Factor in all fees, not just the interest rate.

-

Prepare your application documents. Gather two years of tax returns, recent pay stubs, a current mortgage statement, and a list of all debts with balances and rates.

-

Complete the stress test qualification check. Confirm your TDS ratio stays at or below 44% at the qualifying rate. An Alberta mortgage broker can run this calculation for you before you apply.

-

Close and pay off debts directly. At closing, direct your lawyer to pay creditors from the proceeds. Do not receive the funds personally and then pay debts. Direct payment prevents the money from being spent elsewhere.

-

Take post-closing actions. Reduce credit card limits, set up automatic mortgage payments, and open a dedicated savings account for your emergency fund.

| Step | Key action |

|---|---|

| Equity calculation | Subtract mortgage balance from 80% of appraised value |

| Penalty check | Get written penalty quote from your current lender |

| Payback test | Penalty divided by annual savings; under 18 months is favourable |

| Application prep | Two years of income documents, full debt list, mortgage statement |

| Post-closing | Reduce credit limits, automate payments, build emergency fund |

Key takeaways

Debt consolidation with a mortgage reduces monthly payments but only delivers long-term savings when homeowners control spending, run the payback test, and use accelerated payments to offset extended amortisation.

| Point | Details |

|---|---|

| Know your real equity | Subtract your mortgage balance from 80% of home value to find actual borrowing room. |

| Run the payback test | Divide your prepayment penalty by annual savings; favour refinancing only under 18 months. |

| Secured debt carries higher risk | Rolling unsecured debt into your mortgage puts your home at risk if payments fail. |

| Qualification thresholds matter | A credit score of 680+ and a TDS ratio of 44% or less are standard A-lender requirements. |

| Discipline determines the outcome | Post-consolidation spending habits decide whether consolidation helps or makes things worse. |

What I have learned from watching homeowners use this tool

I have worked with many Alberta homeowners who came to me convinced that consolidating their debt into their mortgage would fix everything. Sometimes it does. Often, the outcome depends less on the rate they get and more on what they do in the six months after closing.

The homeowners who benefit most are the ones who treat consolidation as a reset, not a solution. They close their high-rate credit cards, set up bi-weekly payments, and build a cash buffer before anything else. The ones who struggle are the ones who see the lower monthly payment as freed-up spending room. Within a year, they have rebuilt the credit card balances and now carry a larger mortgage on top of them.

The payback test is the most underused tool in this process. I see homeowners accept refinancing penalties of $12,000 or more without checking whether the interest savings justify the cost. In many cases, a HELOC at a slightly higher rate costs far less overall because there is no penalty to absorb.

My honest advice: do not let the appeal of a lower monthly payment drive the decision. Run the full numbers, including total interest over the life of the loan, all fees, and the penalty. If the math works and you are committed to changing your spending habits, mortgage-backed consolidation is one of the most effective debt relief tools available to Canadian homeowners. If the math is marginal or the discipline is uncertain, a consumer proposal or a structured repayment plan may serve you better.

— Denee

Debt consolidation options with Deneenoel in Alberta

Alberta homeowners dealing with high-interest debt have real options, and the right one depends on your equity, your credit, and your goals. Deneenoel works with over fifty Canadian lenders to find refinancing, HELOC, and second mortgage solutions tailored to your specific situation.

Whether you are in Edmonton, Calgary, or anywhere across Alberta, Deneenoel provides a clear, honest assessment of your consolidation options before you commit to anything. There are no generic recommendations here. Every plan starts with your numbers. Connect with an Edmonton mortgage broker or reach out through Deneenoel's Calgary services to book a no-obligation consultation and find out exactly what your home equity can do for your financial situation.

FAQ

What is debt consolidation with a mortgage?

Debt consolidation with a mortgage combines multiple debts into a single mortgage payment secured by your home equity, typically at a lower interest rate than credit cards or personal loans.

How much home equity do I need to consolidate debt?

You need enough equity so that your total borrowing stays within 80% of your home's appraised value after subtracting your existing mortgage balance.

What credit score do I need to qualify?

Most A-lenders in Canada require a credit score of 680 or higher and a total debt service ratio of 44% or less to approve a refinance or HELOC for debt consolidation.

Is it risky to roll debt into my mortgage?

Converting unsecured debt to secured mortgage debt puts your home at risk if you miss payments. Unlike unpaid credit cards, an unpaid mortgage can lead to foreclosure.

When is a consumer proposal better than mortgage consolidation?

A consumer proposal is the better option when you have poor credit, insufficient home equity, or unstable income that prevents you from qualifying for a refinance or HELOC.